£258 /Month

£2,051 Deposit

6.90% APR

PEUGEOT 208

STYLE 1.2L PURETCH 100 S&S - Agueda Yellow 2

- Petrol

- Manual

PCP finance is similar to hire purchase (HP) but instead of your payments being based on the car’s total value, you pay off its depreciation instead (the difference between what the car is worth now and at the end of the contract)

With this option, you can use the car until your contract ends and at the end of the contract, you have three options.

You can either return the car, pay the resale value, and keep it, or you can use the resale value and put it towards buying a new car. These are the only three options available to you at the end of a PCP contract, so you need to have decided what you’re going to do before the contract comes to a close.

You are likely going to be asked to pass a credit check before you will be accepted for a PCP contract. You’ve got to be able to make these repayments every month, and keep in mind that this kind of contract can last up to four years. So, if you don’t think you’re going to be able to keep up with the payments for the entire contract, you might need to consider something else.

You have three main options to choose from when you come to the end of your agreement. These include:

Consistently making your car finance payments, and even making early payments, can have a positive impact on your credit score over time. Early payments demonstrate your commitment to paying off your debt and can help boost your credit rating. Additionally, having different types of credit, such as a car finance agreement, on your credit report can diversify your credit mix and further improve your credit score

You can end your PCP agreement early in two ways, depending on how much you’ve paid:

If you’ve paid 50% or more of the total amount, you can return the car and end the agreement.

You won’t get any money back and may need to pay for excess mileage or damage.

If you’ve paid less than 50%, you can settle the agreement by paying the remaining balance.

Once paid, the car is yours and you won’t pay any future interest.

Step of 1 of 4

Can I get credit

Please answer a few questions, so we can process your finance application.

Estimated time: 1m

£258 /Month

£2,051 Deposit

6.90% APR

PEUGEOT 208

STYLE 1.2L PURETCH 100 S&S - Agueda Yellow 2

£230 /Month

£3,329 Deposit

5.90% APR

SEAT Ibiza

New SE 1.0 TSI 95 PS

£249 /Month

£249 Deposit

0.00% APR

BYD Dolphin Surf

43.2kWh Boost Hatchback 5dr Electric Auto (87 ps)

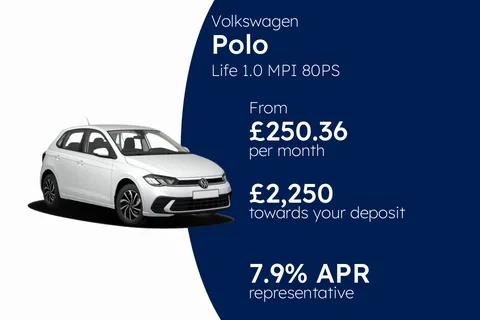

£250 /Month

£3,308 Deposit

7.90% APR

Volkswagen Polo

Life 1.0 MPI 80PS 5-speed Manual 5 Door